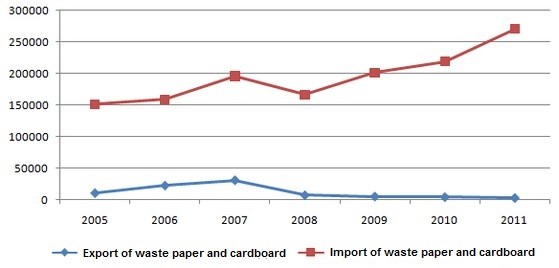

Solid waste situation in Ukraine

For Ukraine, as well as for many other countries, the issue of solid waste treatment is very urgent, considering that accumulated solid waste is the main cause of soil and groundwater pollution. According to the Ministry of Regional Development and Construction (hereinafter – “MRDC”) in Ukraine in 2011 about 12 m tons of municipal solid waste (MSW) were produced, and the annual amount is growing by an average of 3-5% per year. Also, according to MRDC, waste accumulated by this point of time contains about 2.5 m tons of paper, 400 thsd tons of steel, 25 thsd tons of ferrous metals, and 400 thsd t of plastic. In 2011, the UNDP estimated the value of raw material potential in case of introduction of separate waste collection and waste recycling would amount to c. UAH 1.3 bn (about EUR 120 m).

Ukrainian government recognizes importance and urgency of the problem of solid waste treatment in Ukraine and is currently implementing a number of initiatives at the national level – National project “Clean City” (under the patronage of the President of Ukraine) – construction of waste processing plants in 10 regions of Ukraine on terms of public-private partnership.

Solid domestic waste production

According to MRDC, c. 50 m cubic meters of waste are produced annually in Ukraine, or about 11-12 m tons of waste, an average of 240 kg per capita (in large cities this figure may be as high as 400-450 kg/ person). The forecasted growth of MSW production is 3-5% per annum. Also, the Ministry estimates that currently there have been accumulated approximately 2.5 m tons of paper and cardboard, 400 thsd tons of ferrous and 25 thsd tons of non-ferrous metals, and 400 thsd tons of plastic in the form of waste.

According to the analytical study carrid out in 2011 under the UNDP project “Municipal Governance and Sustainable Development”, calculations based on market prices for secondary raw materials in Ukraine resulted in the following estimations of economic effect from operation of waste processing complexes, which incorporate waste sorting stations and incinerators for solid waste: paper and cardboard – UAH 180 m, metals – UAH 225 m, glass – UAH 40 m, polymers – UAH 740 m, textile – UAH 80 m, and heat or electricity generated for the surrounding neighborhoods and waste processing purposes – UAH 35 m. The total effect could amount to UAH 1.3 bn (EUR 120 m).

In 2011 only 7% of household waste was recycled and disposed of (3% – separately collected and recycled, 4% – burned in two incineration plants – in Kyiv and Dnipropetrovsk).

In 9 Ukrainian cities: Kyiv, Sevastopil, Kharkiv, Chernivtsi, Simferopol, Olexandria (Kirovohradska obl.), Novohrad-Volynskyy, Bucha and Pohreby (Kyivska obl.) there are waste sorting lines in operation, and in 19 more towns such facilities are under construction. In two cities (Kyiv and Dnipropetrovsk) waste is partially being utilized at incineration plants, and in Lyubotin (Kharkivska obl.) a pilot incineration plant has been recently put into operation.

Waste treatment plants in Ukraine